Getting approved for a personal loan with bad credit can feel like an uphill battle, but it's not an impossible task. Having a low credit score may narrow your options, but it doesn’t eliminate them entirely. Lenders today understand that credit scores don’t always tell the full story. Whether you’ve faced unexpected expenses, medical emergencies, or financial setbacks, there are still opportunities to secure the funds you need. By understanding how the process works and where to look, you can find loan options tailored to your situation.

In this comprehensive guide, we’ll break down everything you need to know about obtaining a personal loan with bad credit. From understanding what bad credit entails to exploring the types of loans available, this article covers it all. We’ll also provide actionable tips to improve your chances of approval and how to avoid predatory lending practices. Whether you’re looking for a small loan to cover an urgent expense or something more substantial, this guide will equip you with the knowledge to make informed decisions.

Don’t let a low credit score hold you back from achieving your financial goals. With the right approach, you can not only secure a personal loan but also take steps to rebuild your credit over time. Read on as we dive deep into strategies, options, and expert advice to help you navigate the world of personal loans, even with bad credit.

Table of Contents

- What Is Bad Credit?

- How Credit Scores Affect Loan Approvals

- Types of Personal Loans for Bad Credit

- Secured vs. Unsecured Loans

- Eligibility Requirements for Bad Credit Loans

- Steps to Apply for a Personal Loan with Bad Credit

- How to Improve Your Chances of Approval

- Top Lenders to Consider for Bad Credit Loans

- Avoiding Predatory Lenders

- Benefits and Drawbacks of Personal Loans for Bad Credit

- Alternatives to Personal Loans

- How Repaying a Loan Can Impact Your Credit Score

- Tips for Rebuilding Credit After a Loan

- Frequently Asked Questions (FAQs)

- Conclusion

What Is Bad Credit?

Bad credit refers to a low credit score, often caused by missed payments, high credit utilization, or past bankruptcies. Credit scores are numerical indicators of your creditworthiness, typically ranging from 300 to 850. A score below 580 is generally considered poor, according to FICO standards. Poor credit can make it difficult to qualify for loans, credit cards, and even rental agreements.

However, bad credit isn’t a permanent label. It’s a snapshot of your financial history that can be improved over time with responsible financial behavior. Understanding what constitutes bad credit and how it impacts your borrowing ability is the first step toward finding the right personal loan option.

How Credit Scores Affect Loan Approvals

Your credit score is one of the first things lenders look at when evaluating your loan application. It helps them assess the level of risk involved in lending you money. A higher credit score signifies lower risk, which translates to better loan terms, such as lower interest rates and higher borrowing limits. Conversely, a lower credit score means higher perceived risk, often resulting in higher interest rates and stricter loan terms.

When you have bad credit, lenders may be hesitant to approve your loan application outright. However, some lenders specialize in providing personal loans for individuals with bad credit. These loans may come with higher interest rates, but they can serve as a stepping stone to rebuild your financial health.

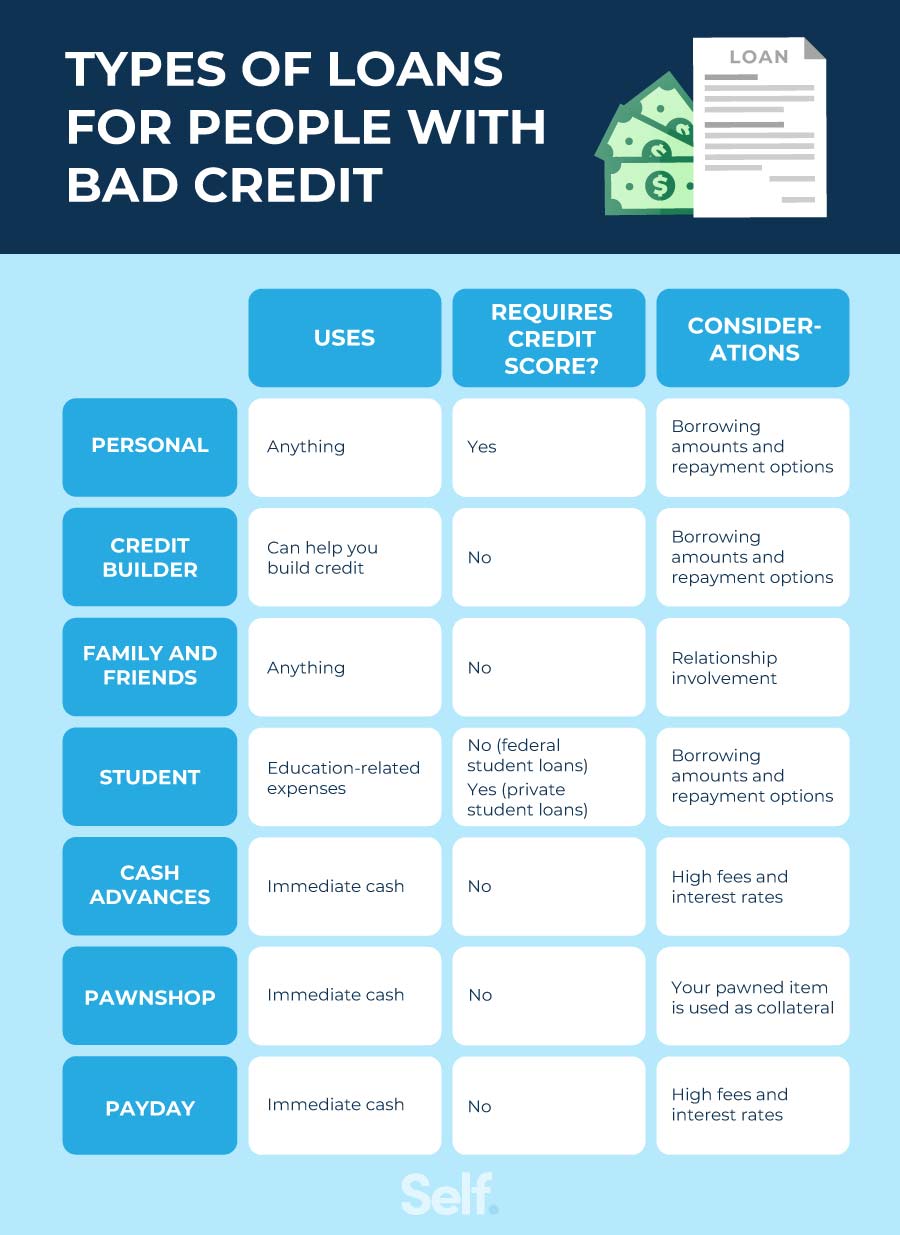

Types of Personal Loans for Bad Credit

There are several types of personal loans available for borrowers with bad credit, each tailored to specific needs:

- Payday Loans: Short-term loans that provide quick cash but often come with extremely high interest rates.

- Installment Loans: Loans repaid in fixed monthly payments over a set period, usually with more manageable terms.

- Title Loans: Loans that require you to use your vehicle as collateral. These are typically high-risk loans due to the potential loss of your vehicle if payments are missed.

- Credit Union Loans: Local credit unions may offer personal loans with more favorable terms for members, even those with bad credit.

Each type of loan has its pros and cons. Understanding these options will help you choose one that aligns with your financial goals while minimizing risks.

Secured vs. Unsecured Loans

When exploring personal loans for bad credit, you’ll encounter two primary categories: secured and unsecured loans.

Secured Loans

Secured loans require collateral, such as a car, savings account, or other valuable assets. Because the lender has the assurance of collateral, these loans often come with lower interest rates and higher approval chances. However, if you fail to repay the loan, the lender can seize your collateral.

Unsecured Loans

Unsecured loans don’t require any collateral. Instead, lenders assess your creditworthiness and income to approve the loan. These loans are riskier for lenders, which often leads to higher interest rates and stricter terms for borrowers with bad credit.

Choosing between a secured and unsecured loan depends on your financial situation and willingness to pledge collateral. Both options have their advantages and should be considered carefully.

Frequently Asked Questions (FAQs)

1. Can I get a personal loan with bad credit and no collateral?

Yes, some lenders offer unsecured personal loans specifically for individuals with bad credit. However, these loans may come with higher interest rates and stricter repayment terms.

2. How can I increase my chances of getting approved?

To improve your chances, focus on providing proof of stable income, reducing existing debt, and working with lenders that specialize in bad credit loans.

3. Are there alternatives to personal loans for bad credit?

Yes, alternatives include borrowing from friends or family, using a credit card, or seeking assistance from local credit unions.

4. Will applying for multiple loans hurt my credit score?

Yes, multiple hard inquiries on your credit report can temporarily lower your credit score. It’s best to research lenders beforehand and apply selectively.

5. What is the typical interest rate for bad credit loans?

Interest rates for personal loans with bad credit can range from 10% to 36%, depending on the lender and loan terms.

6. Can I rebuild my credit with a personal loan?

Yes, repaying a loan on time can help improve your credit score by demonstrating responsible borrowing behavior.

Conclusion

Obtaining a personal loan with bad credit may seem challenging, but it’s far from impossible. By understanding your options, improving your financial habits, and working with the right lenders, you can secure the funds you need while taking steps to rebuild your credit. Remember, the journey toward financial stability is a marathon, not a sprint. With patience, persistence, and informed decision-making, you can achieve your goals and improve your overall financial health.

You Might Also Like

Luxury Escapes Redefined: A Guide To The Inn On Lake SuperiorJacoby Jones Death: Facts, Biography, And Impact

Johnny Crawford Actor: A Timeless Talent In Hollywood

Ultimate Guide To Player Auctions: Opportunities And Strategies

Campana: A Timeless Symbol Of Culture And Significance

Article Recommendations

- Herwin Williams A Visionary Leader In Modern Art And Design

- The Ultimate Guide To The Trex Game Fun Facts History And Tips

- Dominos Pizz A Global Icon In The World Of Pizza